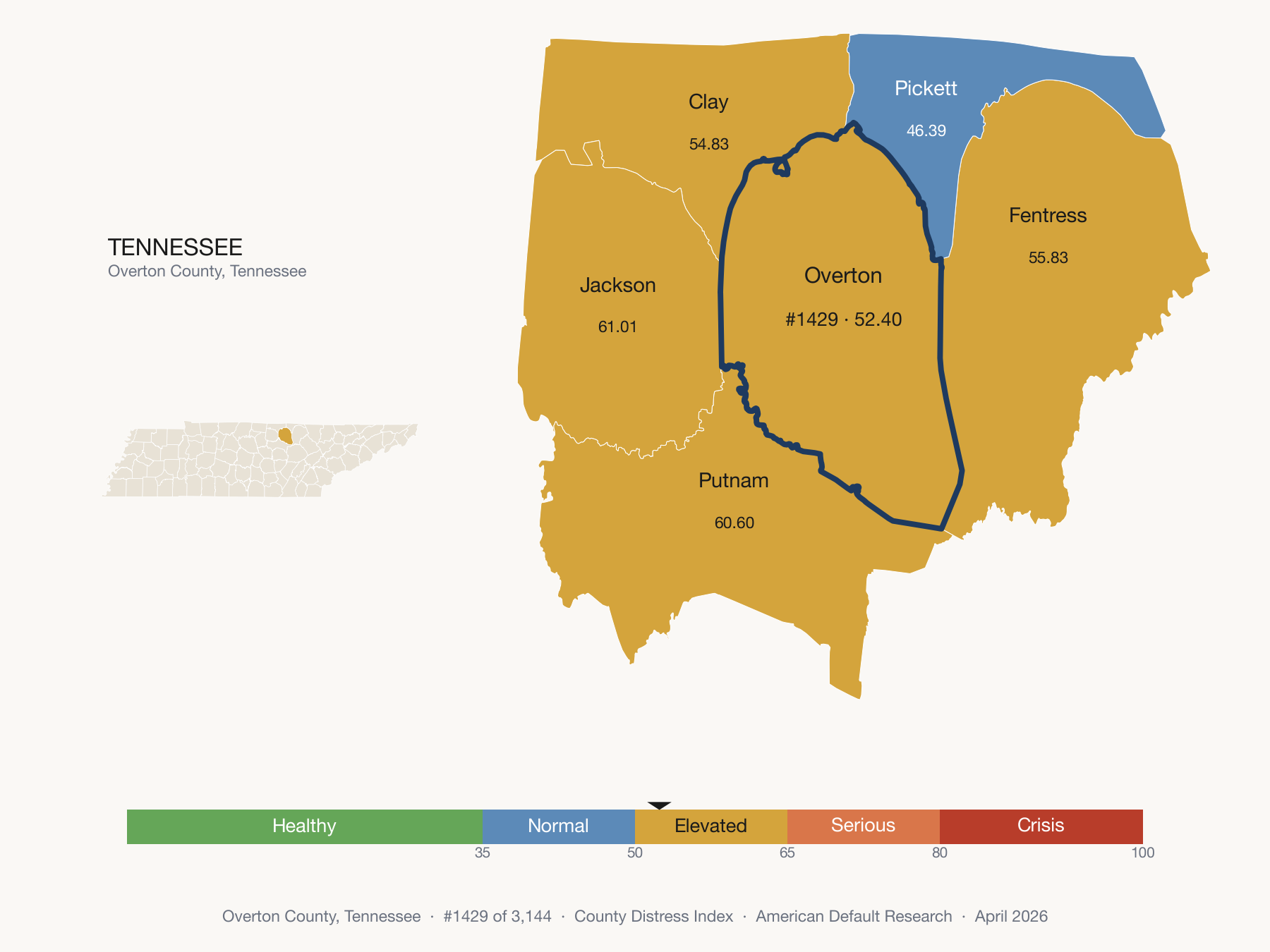

Overton County, Tennessee

Above the national median for bankruptcy filing rate — and 31.1× the rate of the healthiest U.S. county (Glacier County, MT — 7).

Main Findings

Overton County, Tennessee ranks 1,484th most distressed in the United States on the County Distress Index. The driver: a bankruptcy filing rate of 227 — above the national median of 126.

- 1,484th of 3,144 counties on the County Distress Index — Middle fifth, 70th in Tennessee.

- A bankruptcy filing rate of 227 (U.S. median 126). Bankruptcy filing rate at the 81st percentile nationally.

- Transfer-income dependency at 32% — national median 27%, ranked at the 74th percentile.

- Credit card delinquency at 6% — national median 5%, ranked at the 64th percentile.

- Rent-to-income ratio at 21% — national median 21%, ranked at the 51st percentile.

"Overton County ranks in the middle fifth of U.S. counties. The county sits near the national center of the CDI distribution, so the domain mix carries the story."

"The CDI places this county in the middle fifth nationally. The county sits near the center of the geography distribution, so the domain mix matters more than the composite alone."

The Indicators Behind Overton County's CDI Score

Every number traces to a public source. Overton County's value shown alongside TN's median and the U.S. median. Full CSV available for download.

| Indicator | Overton | TN median | U.S. median | Pctile | Source |

|---|---|---|---|---|---|

| Delinquency — domain score 54 · Rank 1,414 of 3,144 | |||||

| Auto loan delinquency Share of auto loan accounts 60+ days past due | 5% | 6% | 5% | 43rd | Urban Institute (2024) |

| Credit card delinquency Share of credit card accounts 60+ days past due | 6% | 6% | 5% | 64th | Urban Institute (2024) |

| Subprime credit share Share of residents with a credit score below 660 | 25% | 26% | 23% | 56th | Urban Institute (2024) |

| Default & Legal — domain score 68 · Rank 797 of 3,144 | |||||

| Debt in collections Share of residents with a credit file who have debt in collections | 24% | 28% | 23% | 55th | Urban Institute (2024) |

| Bankruptcy filing rate Personal bankruptcy filings per 100,000 residents | 227 | 216 | 126 | 81st | US Courts F-5A (2025) |

| Debt Burden (housing basis) — domain score 43 · Rank 1,876 of 3,144 | |||||

| Rent-to-income ratio Fair Market Rent (2BR) as share of median household income | 21% | 22% | 21% | 51st | HUD FMR × Census ACS (2024) |

| Severe rent burden (50%+) Share of renter households paying 50%+ of income on rent | 15% | 17% | 18% | 34th | Census ACS 5-yr (2023) |

| Labor — domain score 31 · Rank 2,191 of 3,144 | |||||

| Unemployment Share of labor force unemployed | 3% | 4% | 4% | 31st | BLS LAUS (Dec 2025) |

| Safety Net & Buffer — domain score 63 · Rank 1,052 of 3,144 | |||||

| Child poverty rate Share of children under 18 below the federal poverty line | 19% | 21% | 18% | 57th | Census SAIPE (2023) |

| Disability rate Share of residents reporting a disability | 18% | 19% | 16% | 70th | Census ACS 5-yr (2023) |

| Poverty rate Share of population below the federal poverty line | 14% | 16% | 14% | 56th | Census SAIPE (2023) |

| Transfer-income dependency Share of personal income from government transfers | 32% | 30% | 27% | 74th | BEA Regional Personal Income (2023) |

| Uninsured rate Share of residents without health insurance coverage | 8% | 10% | 8% | 50th | Census ACS 5-yr (2023) |

Five-Domain Breakdown

The CDI is an equal-weight composite of five family-v1 distress domains. Each domain contributes 20% of the county score.

Methodology

The County Distress Index is a 0–100 composite score of household financial distress, computed for all 3,144 U.S. counties. Higher scores indicate greater distress. The index is built from five equal-weighted domains: Delinquency, Default & Legal, Debt Burden, Labor, and Safety Net & Buffer. Each domain is the mean of distress-oriented indicator percentiles; the CDI score is the equal-weight mean of those domain scores.

Data sources include the Urban Institute Debt in America (Equifax consumer credit panel), U.S. Census Bureau (American Community Survey 5-year, Small Area Income and Poverty Estimates, Business Formation Statistics), Bureau of Labor Statistics (Local Area Unemployment Statistics, Quarterly Census of Employment and Wages), U.S. Courts Administrative Office (F-5A bankruptcy filings), and HUD Fair Market Rents. Data vintages range from 2023 to 2025 depending on source; full indicator-level vintage detail is in the methodology document.

For Press & Research

Everything you need to cite Overton County data — in under 60 seconds.

Draft wire copy 150-word AP-style article — use freely with attribution

LIVINGSTON, Tenn. — Overton County ranks 1,484th among the nation's most financially distressed counties, according to the County Distress Index released this month by American Default Research.

The composite score of 52 out of 100 places Overton in the middle fifth. Among 3,144 U.S. counties scored, 1,483 counties rank more distressed. Within Tennessee, Overton ranks 70th of 95 counties.

The index, which draws on 16 source indicators from the U.S. Census Bureau, Bureau of Labor Statistics, Urban Institute and federal court filings, identifies default & legal as the primary driver in Overton. A bankruptcy filing rate of 227 — above the national median of 126.

"Overton County ranks in the middle fifth of U.S. counties. The county sits near the national center of the CDI distribution, so the domain mix carries the story," said Ross Kilburn, founder of American Default Research.

Full methodology and county-by-county data are available at americandefault.org/methodology/cdi.

Frequently Asked Questions

What is Overton County's CDI score, and what does it mean?

What drives Overton County's distress score?

How does Overton County compare to its neighbors?

How is the County Distress Index calculated?

Overton County resident looking for help? HUD counselors, legal aid, and attorney referrals →