Delinquency Rate on Consumer Loans (ex credit card)

Non-credit-card consumer loan delinquency

What is the current Delinquency Rate on Consumer Loans (ex credit card)?

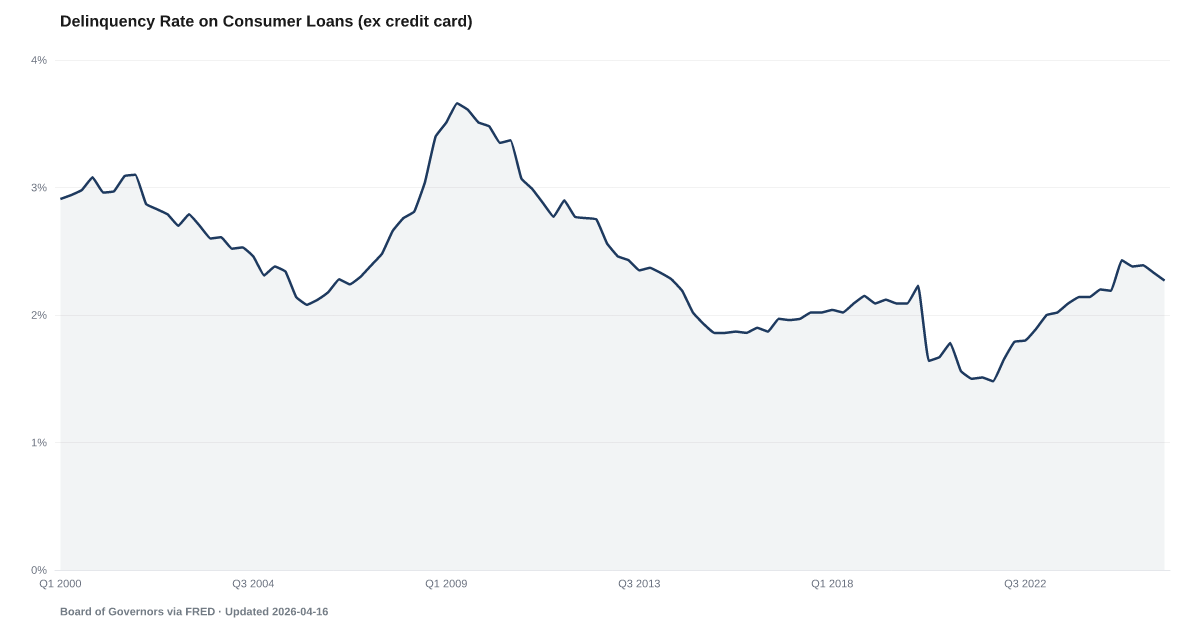

The delinquency rate on consumer loans excluding credit cards — covering auto loans, personal loans, and other non-revolving consumer credit — was 2.3% in Q1 2026, according to the Federal Reserve Board. This measure isolates installment loan performance from the higher-volatility credit card segment, providing a cleaner signal of consumer repayment capacity on fixed-payment obligations like auto loans and personal loans. Source: Federal Reserve via FRED (DROCLACBS).

Non-card consumer loan delinquency has eased to 2.3% from a recent high of 2.43% in Q4 2024 — but remains well above the 1.48% stimulus-era low.

This is the quietest delinquency series in the consumer credit panel. Personal loans, installment loans, point-of-sale loans — everything that isn't a credit card or an auto loan or a mortgage. The Board of Governors reports it quarterly alongside the more-watched card and mortgage series, and it gets cited less often because it's usually boring.

At 2.3% in Q1 2026, the rate has drifted down from a recent high of 2.43% reached in Q4 2024. Read as a recent trend, that's easing. Read against the 1.48% low reached in Q4 2021 during pandemic stimulus, it's still well above — and above the pre-pandemic average of roughly 2%.

The series moves more slowly than credit cards because these loans are smaller and the terms are shorter. The same borrowers running up Credit Card Delinquency are typically also using buy-now-pay-later and personal loans, but those obligations cycle faster — a 6-month installment loan is resolved or written off before a credit card delinquency fully matures.

The modest easing here mirrors the pattern in card delinquency. It sits in the recovery range of a labor market that hasn't yet fully rolled over, with All-Loan Charge-Offs still elevated and Serious Delinquency still climbing on the NY Fed side. The inputs to future delinquency are all still pointing up.

Explore Further

How has Delinquency Rate on Consumer Loans (ex credit card) changed over time?

Most affected counties

Counties with the highest delinquency scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q1 2026 | 2.28% | −0.1 pts |

| Q4 2025 | 2.27% | −0.2 pts |

| Q3 2025 | 2.33% | +0.1 pts |

| Q2 2025 | 2.39% | +0.2 pts |

| Q1 2025 | 2.38% | +0.3 pts |

| Q4 2024 | 2.43% | +0.3 pts |

| Q3 2024 | 2.19% | +0.1 pts |

| Q2 2024 | 2.2% | +0.2 pts |

| Q1 2024 | 2.13% | +0.1 pts |

| Q4 2023 | 2.14% | +0.2 pts |

| Q3 2023 | 2.09% | +0.3 pts |

| Q2 2023 | 2.01% | +0.2 pts |

Frequently Asked Questions

What is the consumer loan delinquency rate excluding credit cards?

The consumer loan delinquency rate excluding credit cards was 2.3% in Q1 2026, per the Federal Reserve Board (FRED series DROCLACBS). This rate covers auto loans, personal loans, and other installment consumer credit at commercial banks, excluding revolving credit card balances.

Why exclude credit cards from consumer loan delinquency?

Credit cards have structurally higher delinquency rates and different payment dynamics than installment loans. Separating them reveals the performance of fixed-payment obligations — auto loans, personal loans — where missed payments more directly signal income disruption rather than revolving balance management.

How does this relate to credit card delinquency?

The all-bank credit card delinquency rate (2.94% in Q1 2026) runs higher because revolving credit is easier to fall behind on. When non-card consumer loan delinquency rises alongside credit card delinquency, it signals broader household payment stress — not just credit card overextension.

How does consumer loan delinquency connect to the American Distress Index?

Consumer loan delinquency is one of four inputs to the American Distress Index's Delinquency domain, alongside mortgage, credit card, and auto loan delinquency. It captures the loan categories the other three miss, so the domain reads household debt performance across the full spectrum of loan types.

Where does this data come from?

The Federal Reserve Board publishes this quarterly as part of its Charge-Off and Delinquency Rates on Loans and Leases at Commercial Banks report. American Default tracks it via the FRED series DROCLACBS, which covers all commercial banks.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…