The Repo Line

Auto loans 90+ days past due as share of total auto debt

What is the current The Repo Line?

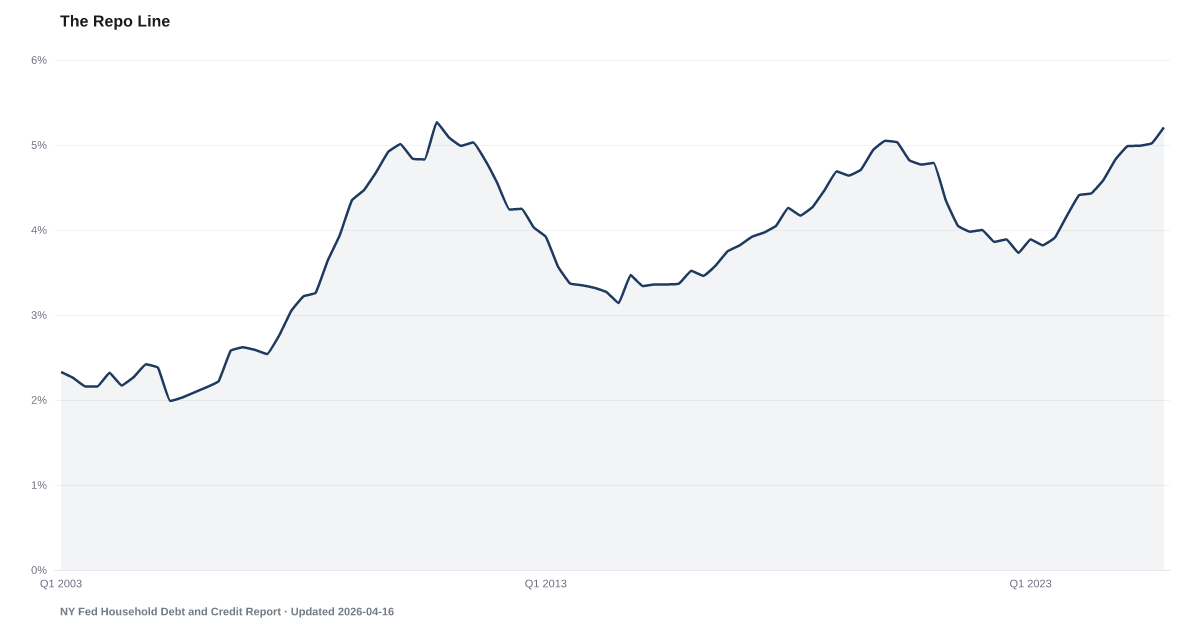

Auto loan serious delinquency — balances 90 or more days past due — reached 5.2% in Q4 2025, according to the New York Fed. This is the highest rate since Q4 2010, during the long tail of the Great Recession, and up from 3.98% at the end of 2021. Unlike mortgages, auto loans received no pandemic forbearance programs, making them an early and unfiltered signal of household financial stress. Source: NY Fed Household Debt and Credit Report (Q4 2025).

The auto loan market has become the clearest signal of what happens when strained borrowers meet elevated borrowing costs.

Serious delinquency on auto loans — balances 90 or more days past due — reached 5.2% in Q4 2025, according to the New York Fed. That is the highest rate since Q4 2010, and up from 3.98% at the end of 2021. Unlike mortgages, where forbearance programs provided a buffer, auto loans received no comparable relief, making them an early and unfiltered signal of household financial stress.

Auto loans occupy a unique position in the household balance sheet. Borrowers typically prioritize car payments above credit cards and even some utility bills, because losing a vehicle means losing the ability to get to work. When auto loan delinquency rises to these levels, it signals that borrowers have already exhausted other options. Falling Behind confirms the broader picture: total delinquency across all consumer debt is rising in step.

The surge in auto loan distress traces directly to the pandemic-era vehicle market. Buyers who purchased vehicles in 2021–2022 paid inflated prices and, as rates rose, locked in higher monthly payments. The Card Tax illustrates the broader rate environment as credit card APRs add to the pressure. For households already managing elevated credit card debt, an underwater auto loan becomes the breaking point. Pink Slips adds another dimension: January 2026 saw the worst start-of-year layoff announcement total in many years, compounding the pressure.

Explore Further

Is this happening to you?

Are you worried about making your next car payment?

How has The Repo Line changed over time?

Most affected counties

Counties with the highest delinquency scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q4 2025 | 5.21% | +0.4 pts |

| Q3 2025 | 5.02% | +0.4 pts |

| Q2 2025 | 4.99% | +0.6 pts |

| Q1 2025 | 4.99% | +0.6 pts |

| Q4 2024 | 4.83% | +0.7 pts |

| Q3 2024 | 4.59% | +0.7 pts |

| Q2 2024 | 4.43% | +0.6 pts |

| Q1 2024 | 4.41% | +0.5 pts |

| Q4 2023 | 4.17% | +0.4 pts |

| Q3 2023 | 3.91% | +0.0 pts |

| Q2 2023 | 3.82% | −0.0 pts |

| Q1 2023 | 3.89% | −0.1 pts |

Frequently Asked Questions

What is the current auto loan delinquency rate?

5.2% of auto loan balances were 90 or more days past due in Q4 2025, according to the New York Fed. This is the highest serious delinquency rate since Q4 2010 and is up from 3.98% at the end of 2021.

Why is auto loan delinquency a leading distress signal?

Borrowers typically prioritize car payments above credit cards and even some utility bills because losing a vehicle means losing the ability to get to work. When auto loan delinquency rises to these levels, it signals that borrowers have already exhausted other options and are in severe financial distress.

What is driving the increase in auto loan delinquency?

Buyers who purchased vehicles in 2021–2022 paid inflated prices and, as rates rose, locked in higher monthly payments. Combined with a record 20.97% average credit card APR and depleted savings (personal savings rate at 3.6%), many households cannot keep up with auto loan payments.

How does auto delinquency compare across income levels?

Auto loan distress is heavily concentrated among subprime borrowers, who faced both higher vehicle prices and higher financing rates. Auto loans received no comparable pandemic relief to mortgage forbearance, making them an unfiltered measure of financial stress without government cushioning.

Where does auto loan delinquency data come from?

The New York Fed reports auto loan delinquency rates quarterly in its Household Debt and Credit Report, based on Equifax credit report data. Auto loan delinquency is one of four inputs to the American Distress Index's Delinquency domain, scored against its own quarterly history since 2005.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…