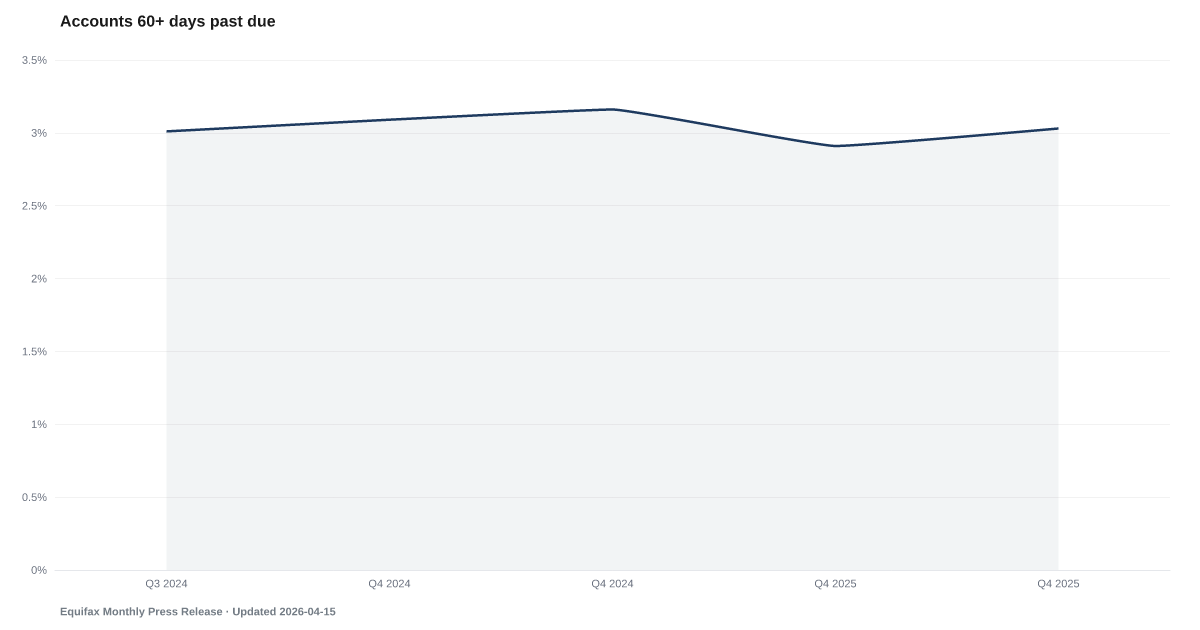

The 60-Day Line

Up from 2.91% last quarter; bankcard 60+ day delinquency still climbing

What is the current The 60-Day Line?

Equifax Monthly Credit Trends tracks early-stage delinquency transitions across consumer credit portfolios, providing a near-real-time view of payment deterioration. The 60-day delinquency marker is a critical threshold — accounts that reach 60 days past due have a substantially higher probability of progressing to charge-off than those at 30 days. Source: Equifax credit data.

The share of credit card balances 60 days past due has settled near the top of its recorded range and refuses to retreat.

Thirty days late is a mistake. Sixty days late is a pattern.

That is the line Equifax tracks each month — the share of bank card balances where a single missed payment has become two, where the servicer's autodialer starts and the late fees compound on the late fees. Equifax's monthly 60+ day series began in September 2024, so long historical comparisons have to come from the broader Federal Reserve credit card series. As of Q4 2025, the Equifax rate sat at 3%, well above the 1.53% stimulus-era low on the comparable Federal Reserve series.

The stall matters. Credit Card Delinquency on bank-reported accounts has eased since 2024. The 60-day share has not eased in parallel. That gap means the accounts that do go late are staying late longer — short cures are giving way to long slides.

The next station down the pipeline is Credit Card Charge-Offs, where the bank declares the balance uncollectable and writes it off as a loss. Credit card charge-offs are running at multi-year highs, with the longest stretch of elevated write-offs since the post-GFC period of 2011–2012. Sixty days is the bridge between the two. It's not a comfortable place to sit.

Explore Further

Is this happening to you?

Have any of your accounts gone 60 or more days past due?

How has The 60-Day Line changed over time?

Most affected counties

Counties with the highest delinquency scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q4 2025 | 3.03% | −0.1 pts |

| Q4 2025 | 2.91% | −0.2 pts |

| Q4 2024 | 3.16% | — |

| Q4 2024 | 3.09% | — |

| Q3 2024 | 3.01% | — |

Frequently Asked Questions

What does the 60-day delinquency line measure?

It tracks the share of consumer credit accounts that have transitioned to 60+ days past due. The 60-day mark is significant because accounts reaching this stage have a substantially higher probability of progressing to charge-off (total loss) than those at only 30 days past due.

Why is 60 days a critical threshold?

At 30 days past due, many borrowers recover. At 60 days, the probability of recovery drops sharply and the likelihood of eventual charge-off or collections increases significantly. The 60-day line is where temporary cash-flow problems become entrenched delinquency.

Where does this data come from?

Equifax publishes monthly credit trend data from its consumer credit database. As one of the three major credit bureaus, Equifax covers hundreds of millions of consumer credit accounts.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…