Student Loan Payment Burden (% of Discretionary Income)

Up from 16.0% a year ago, one of every five dollars earned

What is the current Student Loan Payment Burden (% of Discretionary Income)?

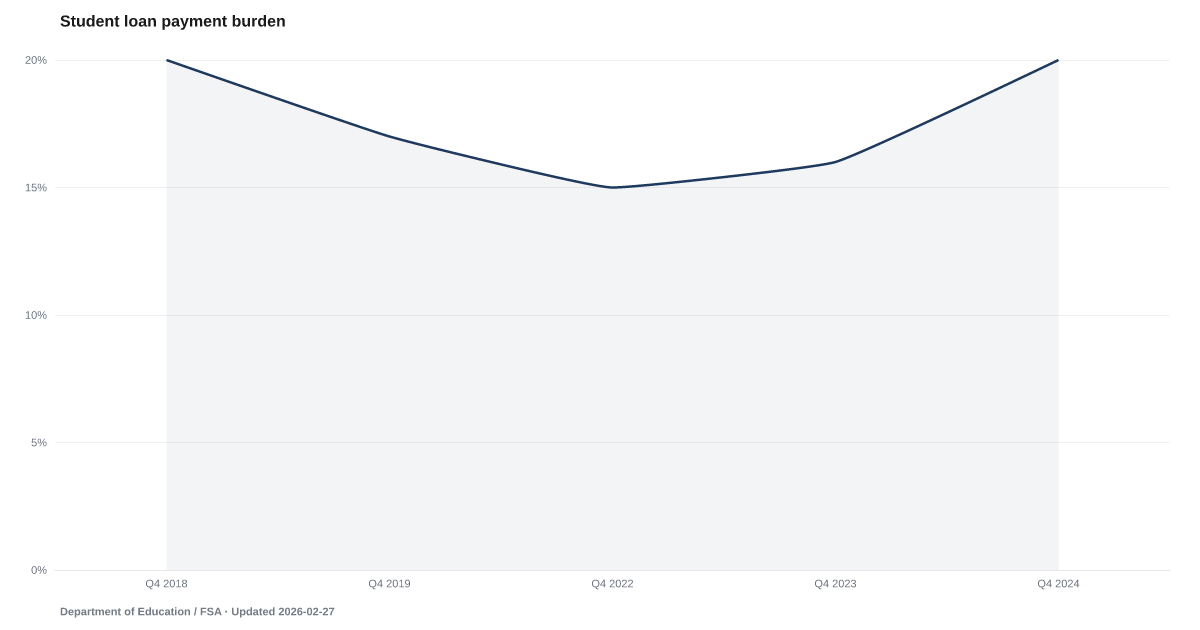

Student Loan Payment Burden (% of Discretionary Income): 20% as of 2024, and worsening. Source: Department of Education / FSA.

Student loan payments now consume 20% of discretionary income for borrowers in active repayment — back to the 2018 burden level after the pause ended.

Federal Student Aid data shows borrowers in active repayment now spend 20% of their discretionary income on student loan payments in 2024. That matches the 2018 reading. In between, the payment pause held the reported burden near 15%. The pause was a mute button. The underlying obligation remained, the reporting paused.

The restart in October 2023 was followed by a 12-month on-ramp during which missed payments would not be reported to credit bureaus. That grace period has ended. The burden that was always there surfaces in every monthly draft.

Twenty cents of every discretionary dollar — money taken before rent, before groceries, before the credit card minimum. The burden ratio measures the squeeze on those still making payments. The share of borrowers actually behind is a separate metric, tracked elsewhere.

Student loans do not discharge in bankruptcy, except under extreme hardship standards most filings never meet. Once a borrower falls into default, wages and tax refunds can be garnished. Falling Behind tracks delinquency across consumer credit broadly. Student loans are the category where delinquency has the hardest landing. The Squeeze gets tighter for every household paying one.

Explore Further

How has Student Loan Payment Burden (% of Discretionary Income) changed over time?

Most affected counties

Counties with the highest debt burden scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| 2024 | 20% | +4.0 pts |

| 2023 | 16% | +1.0 pts |

| 2022 | 15% | — |

| 2019 | 17% | −3.0 pts |

| 2018 | 20% | — |

Frequently Asked Questions

What is Student Loan Payment Burden (% of Discretionary Income)?

Up from 16.0% a year ago, one of every five dollars earned

Why does Student Loan Payment Burden (% of Discretionary Income) matter for financial distress?

Student Loan Payment Burden (% of Discretionary Income) is one of the indicators tracked by the American Distress Index (ADI), which measures five dimensions of U.S. household financial distress: Delinquency, Default & Legal, Debt Burden, Labor, and Safety Net & Buffer. Changes in this indicator contribute to the overall distress picture.

Where does the Student Loan Payment Burden (% of Discretionary Income) data come from?

This data comes from Department of Education / FSA. More information: https://studentaid.gov/data-center/student/portfolio. The American Distress Index updates this indicator annual.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…