Plastic Ceiling

Total revolving consumer credit outstanding

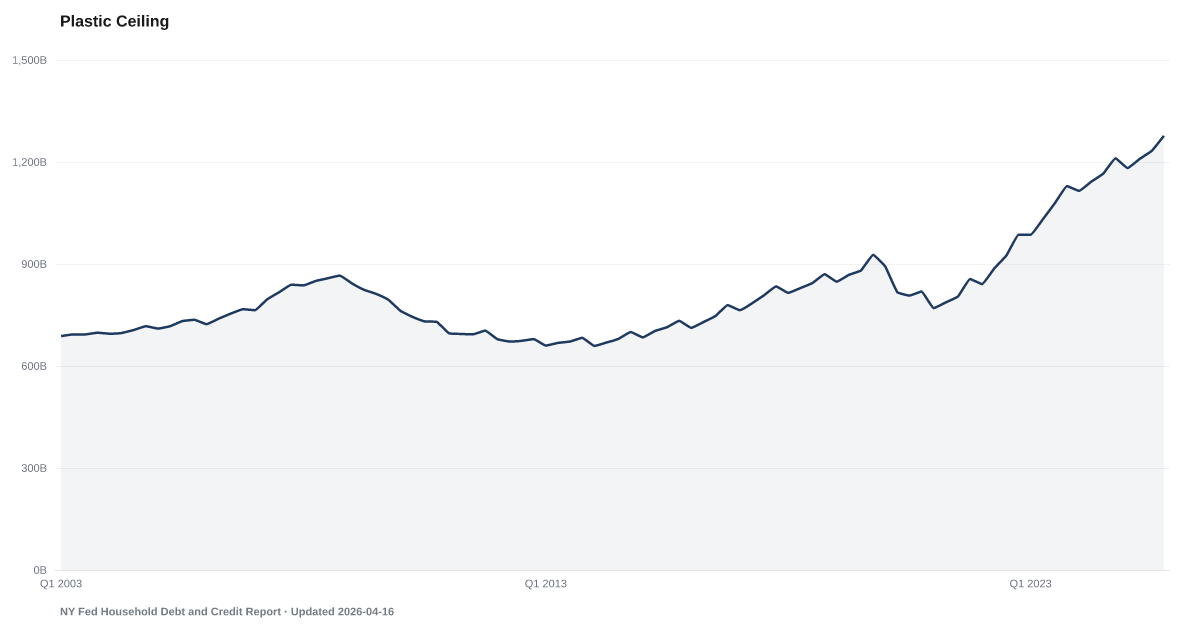

What is the current Plastic Ceiling?

Total U.S. credit card debt reached $1.277 trillion in Q4 2025, according to the New York Fed's Household Debt and Credit Report — a new all-time high, extending a streak of quarterly records. Balances have risen from $856 billion at the end of 2021 to current levels, an increase of over $400 billion in four years representing the fastest credit card debt accumulation on record. Source: NY Fed Household Debt and Credit Report (Q4 2025).

Credit card debt has reached a record high, while carrying that debt remains expensive.

Total credit card balances reached $1277B in Q4 2025, according to the New York Fed's Household Debt and Credit Report — a new all-time high. Balances have climbed from $856 billion at the end of 2021 to current levels, even with the typical Q1 seasonal dip each year. The accumulation since 2021 is unusually steep in the site series.

What makes this buildup different from previous periods is the cost of carrying it. The Card Tax shows the average credit card APR still elevated in the Federal Reserve series. At that rate, a household carrying the average balance pays over a thousand dollars per year in interest alone — money that services debt rather than building savings or covering expenses.

The downstream effects are already visible. Falling Behind shows total delinquency back at pre-pandemic levels, and The Buffer reveals a personal savings rate near multi-decade lows, meaning fewer households have the resources to pay down balances. Elevated debt at elevated interest rates with depleted savings is a combination that hasn't appeared in the data before.

Explore Further

Is this happening to you?

Is your total credit card balance higher than it was a year ago?

How has Plastic Ceiling changed over time?

Most affected counties

Counties with the highest safety net and buffer scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q4 2025 | $1.3T | +$66.0B |

| Q3 2025 | $1.2T | +$67.0B |

| Q2 2025 | $1.2T | +$67.0B |

| Q1 2025 | $1.2T | +$67.0B |

| Q4 2024 | $1.2T | +$82.0B |

| Q3 2024 | $1.2T | +$87.0B |

| Q2 2024 | $1.1T | +$111.0B |

| Q1 2024 | $1.1T | +$129.0B |

| Q4 2023 | $1.1T | +$143.0B |

| Q3 2023 | $1.1T | +$154.0B |

| Q2 2023 | $1T | +$144.0B |

| Q1 2023 | $986B | +$145.0B |

Frequently Asked Questions

How much credit card debt do Americans owe?

Americans owed $1.277 trillion in credit card debt as of Q4 2025, according to the New York Fed's Household Debt and Credit Report. This is an all-time record, having risen from $856 billion at the end of 2021.

How fast is credit card debt growing?

Credit card balances have increased by over $400 billion in four years (2021–2025), the fastest accumulation on record. Balances have risen every quarter during this period, with no signs of the pace slowing.

Why is record credit card debt a problem now?

What makes the current buildup different from previous periods is the cost of carrying it. The average credit card APR stands at 20.97%, the highest ever recorded. At that rate, a household carrying the average balance pays over $1,000 per year in interest alone — money that services debt rather than covering expenses or building savings.

How much of credit card debt is delinquent?

Total delinquency across all consumer debt has risen to 4.8% as of Q4 2025. Credit card-specific delinquency is higher, particularly at smaller banks where it reaches 6.62% — more than double the rate at the largest banks.

Where does the credit card debt data come from?

The New York Fed's Quarterly Report on Household Debt and Credit provides total credit card balance data based on a nationally representative sample from Equifax consumer credit reports. It is released approximately two months after each quarter ends.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…