The Squeeze

Up from 23.7% a year ago, almost nothing left after necessities

What is the current The Squeeze?

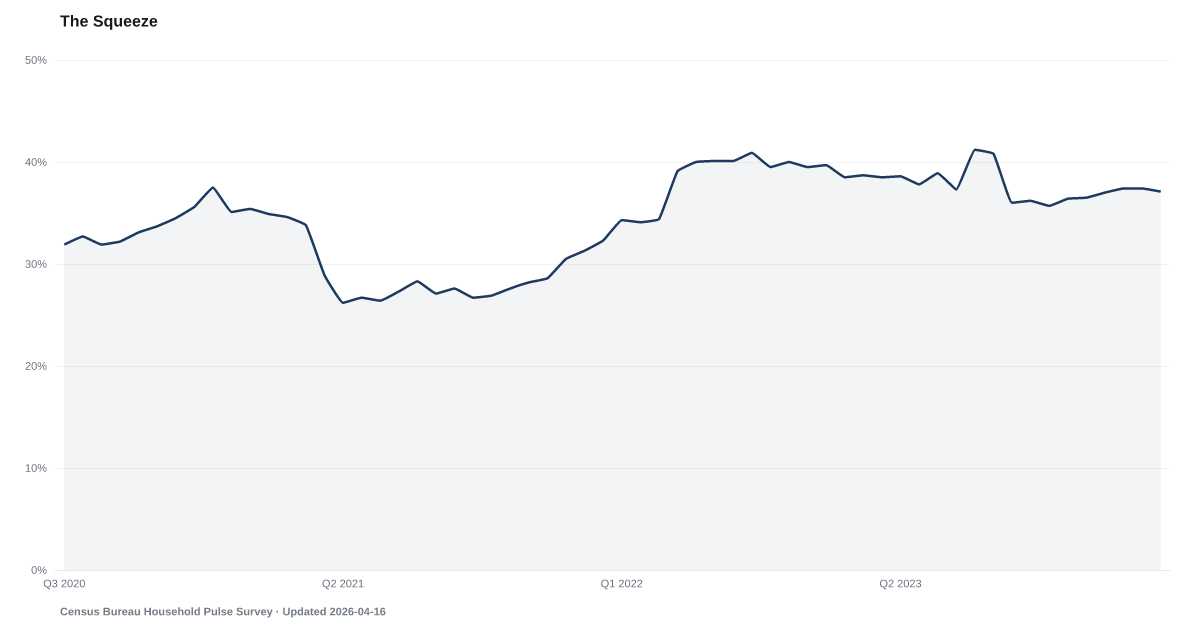

24.0% of U.S. households now spend 95% or more of their income on necessities, according to Bank of America Institute analysis of internal depositor data — up from 23% in 2023. Among lower-income households, the figure is 29%, the highest in the series. These are families with no discretionary spending left to cut and no margin for any unexpected expense. Source: Bank of America Institute (2025).

The gap between what families earn and what they must spend has narrowed to almost nothing for a growing share of households.

Bank of America Institute analysis of internal depositor data shows that 24% of U.S. households now spend 95% or more of their income on necessities — up from 23% in 2023. Among lower-income households the share is higher still and keeps setting new highs in this series. For these families, discretionary spending is no longer a category. Necessities are taking everything.

The driver is visible in The K-Shape: lower-income wages are growing well below inflation, while higher-income households see wage growth that runs comfortably ahead of prices. The K-shaped recovery has become a permanent feature of the economy rather than a temporary post-pandemic artifact.

When nearly every dollar is spoken for, any unexpected expense becomes a crisis. The Buffer shows the personal savings rate well below its pre-pandemic average, and The $400 Test confirms that more than a third of Americans still cannot cover even a minor emergency with cash. These are three views of the same squeeze.

Explore Further

Is this happening to you?

Do you run out of money before your next paycheck arrives?

How has The Squeeze changed over time?

Most affected counties

Counties with the highest safety net and buffer scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| 2025 | 24% | +0.3 pts |

| 2024 | 23.7% | +0.7 pts |

| 2023 | 23% | — |

Frequently Asked Questions

What share of Americans spend nearly all their income on necessities?

24.0% of U.S. households spend 95% or more of their income on necessities, according to Bank of America Institute data. Among lower-income households, the figure is 29%. These households have virtually no discretionary spending or savings capacity remaining.

Is the income-to-necessity ratio getting worse?

Yes. The share of households spending 95%+ on necessities rose from 23% in 2023 to 24.0% in 2025. Among lower-income households specifically, the figure climbed from 27.1% to 29%. The trend is driven by essential costs (groceries, housing, insurance) rising faster than wages for lower-income workers.

Why do households have no margin even when employment is high?

The pressure is coming from the cost side, not employment. Lower-income wage growth is approximately 1% while inflation runs at approximately 3%, creating a negative real wage gap. Higher-income households see 4% wage growth — comfortably ahead of prices — creating a K-shaped divergence where employment statistics mask deepening distress at the bottom.

How does this connect to savings and debt indicators?

When nearly every dollar is consumed by necessities, there is nothing left to save or to use for debt repayment. This directly explains why the personal savings rate has fallen to about 4%, why 37% of adults can't cover a $400 emergency, and why 4.8% of 401(k) participants are taking hardship withdrawals. These are not separate problems — they are three views of the same squeeze.

Where does the income-to-necessity spending data come from?

Bank of America Institute analyzes aggregated and anonymized internal depositor transaction data to measure household spending patterns. This proprietary dataset provides near-real-time insights into consumer financial behavior at scale, making it one of the few sources that can track spending-to-income ratios across income levels.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…