Total Revolving Credit Outstanding

Total revolving credit (primarily credit cards) outstanding

What is the current Total Revolving Credit Outstanding?

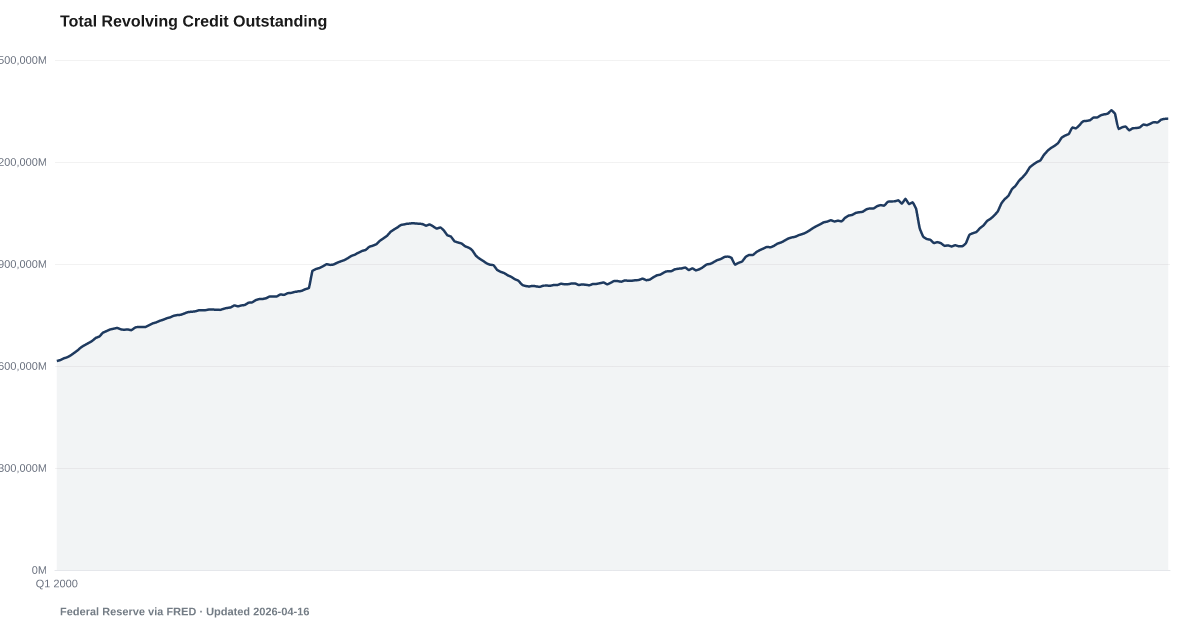

Total Revolving Credit Outstanding: $1.3T as of 2026-04, and worsening. Source: Federal Reserve via FRED.

Revolving credit balances reached $1.4T in October 2024 and remain roughly flat vs that level.

The Federal Reserve's revolving credit series, FRED REVOLSL, tracks credit cards and other revolving consumer loans. The series sits well above the December 2019 reading of roughly $1.09 trillion — most of that growth concentrated since early 2022, when balances began climbing quarter after quarter. The current April 2026 reading is roughly flat vs the October 2024 reference reading.

Revolving credit is the most expensive consumer debt in the system. Average credit card APRs sit above 22%. Unlike a mortgage or an auto loan, the balance is open-ended. A household that can't pay in full in a given month carries it to the next one and accrues interest at the card's rate — regardless of what the Fed has done to the overnight rate.

The composition of the growth matters. Some of it is the natural drift of a growing economy. More of it is households using revolving credit to bridge gaps income isn't closing on its own. When the savings rate runs near historic lows and essential costs keep rising, the card becomes the month-to-month balancing line.

Revolving credit growth this persistent tends to precede waves of delinquency. Falling Behind has already turned upward. Revolving Credit Utilization 75Th Percentile shows stretched borrowers using more than 50% of their available credit — far above the 30% threshold lenders use as a warning. At some point, the card runs out of room. What happens after is what The Safety Net tells us a majority of households cannot absorb on their own.

Explore Further

How has Total Revolving Credit Outstanding changed over time?

Most affected counties

Counties with the highest safety net and buffer scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Apr 2026 | $1.3T | +$49.6B |

| Mar 2026 | $1.3T | +$44.2B |

| Feb 2026 | $1.3T | +$22.4B |

| Jan 2026 | $1.3T | +$23.9B |

| Dec 2025 | $1.3T | +$27.4B |

| Nov 2025 | $1.3T | −$25.5B |

| Oct 2025 | $1.3T | −$35.1B |

| Sep 2025 | $1.3T | −$29.8B |

| Aug 2025 | $1.3T | −$32B |

| Jul 2025 | $1.3T | −$27.1B |

| Jun 2025 | $1.3T | −$29.1B |

| May 2025 | $1.3T | −$31.6B |

Frequently Asked Questions

What is Total Revolving Credit Outstanding?

Total revolving credit (primarily credit cards) outstanding

Why does Total Revolving Credit Outstanding matter for financial distress?

Total Revolving Credit Outstanding is one of the indicators tracked by the American Distress Index (ADI), which measures five dimensions of U.S. household financial distress: Delinquency, Default & Legal, Debt Burden, Labor, and Safety Net & Buffer. Changes in this indicator contribute to the overall distress picture.

Where does the Total Revolving Credit Outstanding data come from?

This data comes from Federal Reserve via FRED. More information: https://fred.stlouisfed.org/series/REVOLSL. The American Distress Index updates this indicator monthly.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…