Delinquency Rate on Single-Family Residential Mortgages (90+ days)

Mortgage loans 90+ days past due

What is the current Delinquency Rate on Single-Family Residential Mortgages (90+ days)?

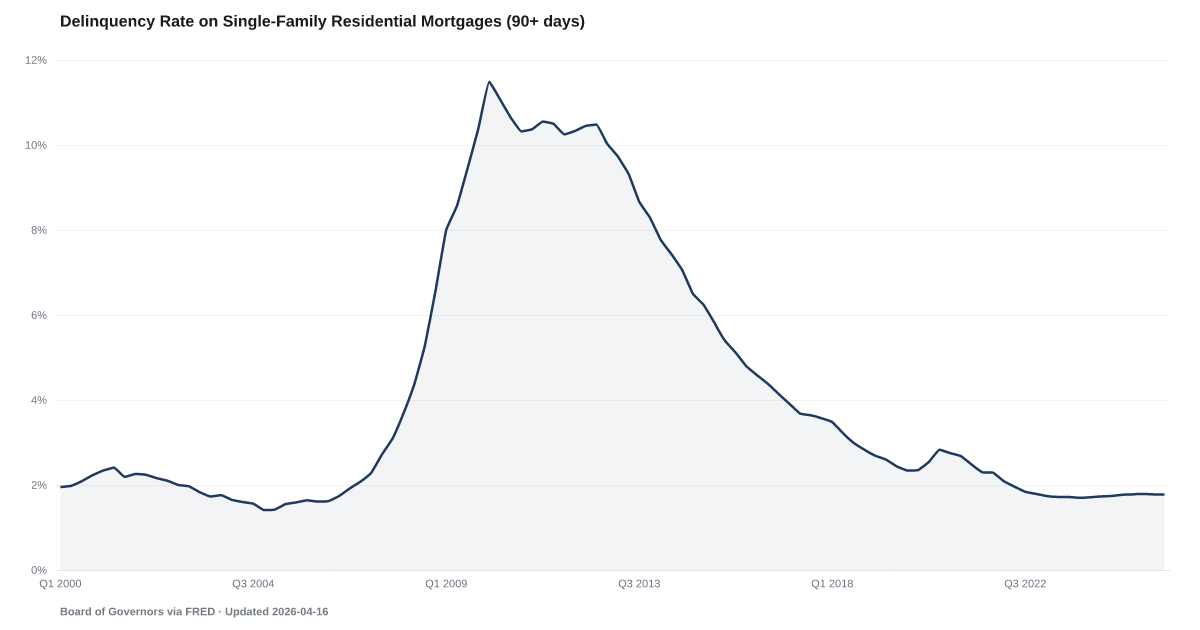

The serious mortgage delinquency rate on single-family residential loans was 1.9% in Q1 2026, according to the Federal Reserve Board (FRED series DRSFRMACBS). This measures loans 90+ days past due at all commercial banks — the threshold where foreclosure proceedings typically begin. The current rate is stable and well below the 11.4% crisis peak in Q1 2010, but represents the conventional mortgage universe only. FHA-insured loans, tracked separately, show 11.52% delinquency — a 6.5x multiplier that the blended national rate obscures. Source: Board of Governors via FRED (DRSFRMACBS).

Mortgage serious delinquency sits at 1.9% in Q1 2026 — historically low, and the quietest data point in the distress picture.

This cycle's distress is showing up almost everywhere except the mortgage book. That's the headline of the data, and it's the point.

The Board of Governors' 90-day mortgage delinquency rate reads 1.9% in Q1 2026, and has held in a narrow band since Q1 2023. That is a historically quiet range. Today's reading is roughly one-sixth of the GFC-era high set in January 2010.

The explanation is vintage, not household health. The mortgage book is mostly old. Mortgage Originations are running well below the 2021 pace. Homeowners locked in at 3% rates are not selling, not refinancing, and not defaulting — the payment is manageable because it was underwritten in a different universe. The distress that would otherwise show up here is landing in Credit Card Delinquency, in Auto Loan Serious Delinquency, and in Credit Card Charge-Offs.

A rate-locked mortgage book is unusually stable. It is also blind to what's happening to the newer borrowers — the FHA buyers, the recent originations — who do not have the 3% buffer protecting them. First Missed is the series to watch. It has already ticked back up from its 2025 low.

Explore Further

How has Delinquency Rate on Single-Family Residential Mortgages (90+ days) changed over time?

Most affected counties

Counties with the highest delinquency scores in the County Distress Index.

Explore all 3,144 counties →| Period | Value | YoY Change |

|---|---|---|

| Q1 2026 | 1.89% | +0.1 pts |

| Q4 2025 | 1.79% | +0.0 pts |

| Q3 2025 | 1.78% | +0.0 pts |

| Q2 2025 | 1.78% | +0.1 pts |

| Q1 2025 | 1.77% | +0.1 pts |

| Q4 2024 | 1.78% | +0.1 pts |

| Q3 2024 | 1.74% | +0.0 pts |

| Q2 2024 | 1.73% | +0.0 pts |

| Q1 2024 | 1.71% | −0.0 pts |

| Q4 2023 | 1.7% | −0.1 pts |

| Q3 2023 | 1.72% | −0.1 pts |

| Q2 2023 | 1.72% | −0.2 pts |

Frequently Asked Questions

What is the current mortgage delinquency rate?

The serious mortgage delinquency rate (90+ days past due) on single-family residential loans at commercial banks was 1.9% in Q1 2026, per the Federal Reserve Board (FRED DRSFRMACBS). This covers conventional mortgages held by commercial banks — not FHA-insured loans, which are tracked separately.

Why does FHA delinquency matter more than the headline rate?

FHA-insured mortgage delinquency was 11.52% in Q1 2026 — 6.5 times the conventional rate of 1.9%. FHA borrowers are predominantly first-time buyers with lower incomes and smaller down payments. Their delinquency rate is a leading indicator of broader default trends because they are the first to feel economic pressure.

How does mortgage delinquency connect to the American Distress Index?

Mortgage delinquency is one of four inputs to the American Distress Index's Delinquency domain, alongside credit card, consumer loan, and auto loan delinquency. Each input is scored against its own quarterly history since 2005. The current conventional rate sits low in that record, and the domain score states exactly how low.

{kind=link}

{kind=link}

Quick poll

Is this affecting you or your household?

Discussion

Get the numbers when they move.

New data drops, indicator updates, and ADI score changes — delivered when it matters. No spam.

or Create an Account for full access

Loading comments…